Featured

Mid-2025 U.S. Real Estate Editorial: Interpreting a Market in Transition

Jon Granston | June 20, 2025

Jon Granston | June 20, 2025

Migration Report

1. Mixed Market Movement

Markets like Florida, Colorado, Washington, D.C., and California have recently seen modest value declines, while cities such as San Jose, Syracuse, Hartford, Bridgeport, and San Diego are quietly climbing. The result? A market that’s recalibrating, not collapsing.

2. Inventory Rising, But Not Everywhere

A loosening of the "lock-in effect" has nudged more homeowners into the market, particularly in states like Arizona, Utah, Texas, and Oregon. Some markets are nearing pre-pandemic inventory levels for the first time in years.

3. Affordability Remains a Barrier

Borrowing power is still constrained. Inventory may be up, but affordable inventory is not—especially in entry-level brackets. High interest rates and inflation-adjusted costs continue to pressure first-time buyers.

4. Mortgage Rates Still Control the Narrative

With 30-year fixed rates hovering near 6.75%, activity remains sensitive to even small movements. Analysts suggest that a meaningful buyer resurgence may not take hold until rates drop closer to—or below—6%.

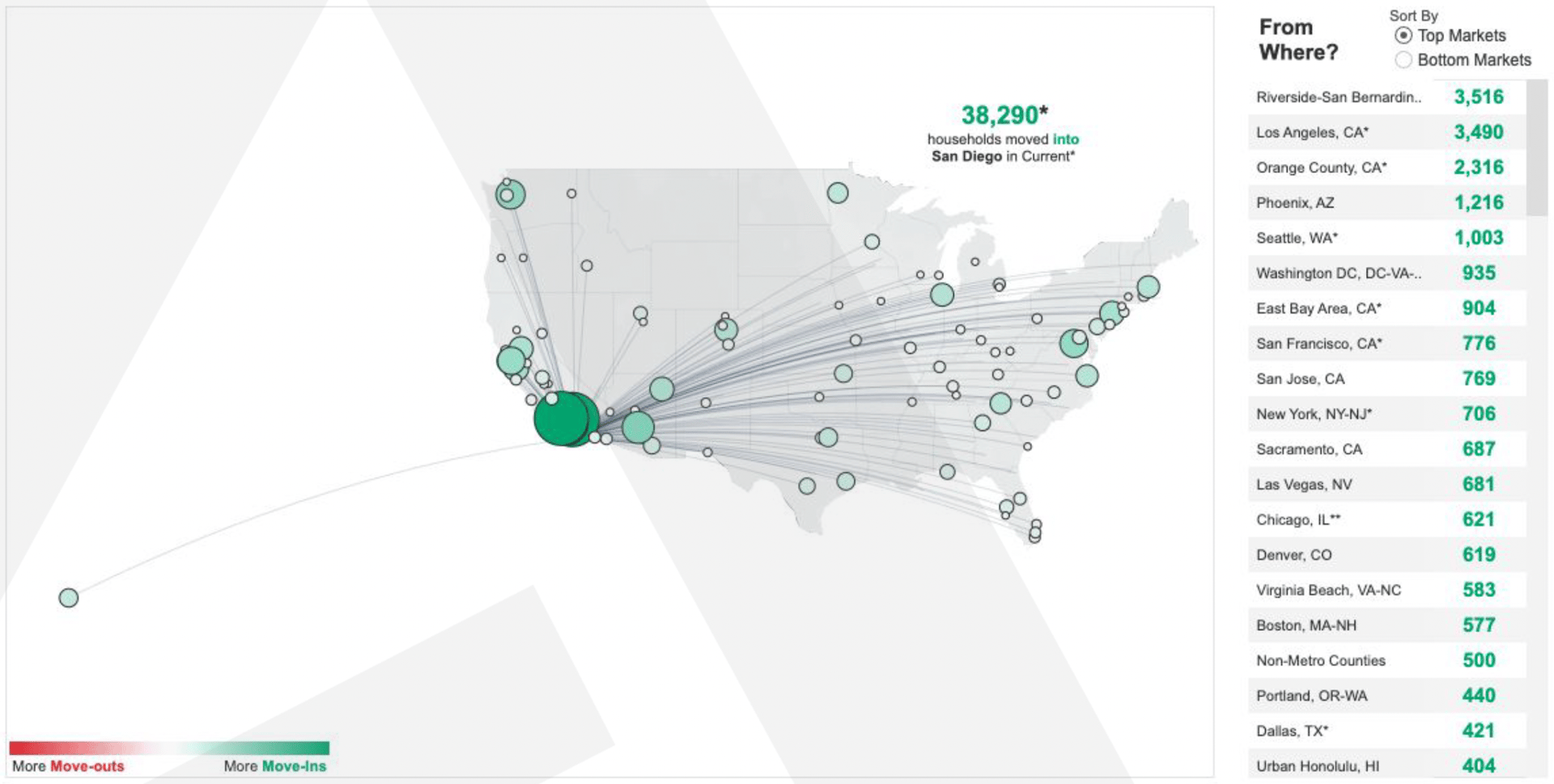

5. Relocation Over Renovation

Over 38% of buyers are now searching outside of their home metro area. Migration is no longer a pandemic trend—it’s become a lifestyle imperative. Tax policy, climate stability, quality of life, and remote work flexibility are driving metro-to-metro shifts in a way that will define the next decade of real estate.

Tariffs on steel, aluminum, and lumber are increasing construction costs by up to $12,000 per home.

A recent 5% dip in the S&P 500, tied to tariff anxieties, sent brief shockwaves through affluent buyer segments—particularly those reliant on portfolio wealth.

Economic uncertainty is softening buyer urgency and increasing “wait-and-see” behavior in many markets.

Despite national headwinds, the San Diego luxury market continues to hold its footing.

In Rancho Santa Fe, the median home price hovers around $4.2M, with price-per-square-foot data averaging $1,050–$1,200, depending on lot size and location.

Coastal North County markets like Del Mar, Encinitas, and Solana Beach remain close to all-time highs. San Marcos recently reached a new record with detached homes averaging $1.34M.

While inventory has increased modestly, buyer demand remains selective—favoring move-in-ready, well-located, and lifestyle-aligned properties.

Over the past five years, Los Angeles County has accounted for the majority of inbound migration to San Diego County, particularly in the luxury tier. That trend is poised to continue.

Drivers of LA-to-SD Migration:

Measure ULA (“Mansion Tax”): The 4–5.5% transfer tax on sales over $5M in LA has shifted buying power south. San Diego offers similar lifestyle appeal—without the tax burden.

Wildfire Fatigue: While San Diego also faces environmental risks, the catastrophic damage in Malibu, the Palisades, and inland valleys has prompted affluent LA homeowners to consider alternative markets such as Orange County, Santa Barbara—and increasingly, San Diego.

Civic Unrest: Recent ICE protests and civil tension in parts of LA have raised lifestyle and security concerns among affluent residents, fueling interest in San Diego’s more balanced pace.

2025 is not a buyer’s market or a seller’s market—it’s a strategic market. One that demands nuanced analysis, local fluency, and a pulse on how broader forces—from tariffs to taxes—shape real estate decision-making. For agents and clients alike, the advantage lies in interpretation, not speculation.